Australian journalist Giles Parkinson has published a must-read series of articles on his website Reneweconomy about how renewable energy is upsetting the business model of incumbent network operators and generators in Queensland, Australia. His insights provide crucial lessons for utilities elsewhere, most certainly in Europe. As a recent report from Citi notes: “If we look at the situation facing European utilities, the future looks particularly challenging.”

Photo by Cafeyak.com

“Like Bob Dylan’s immortal classic ‘The Times They Are a-Changin’ so is the purpose of the electricity distribution network.”

These words, written by the CEO of Queensland-based network operator Ergon Energy, could not fail to attract the attention of the Australian journalist Giles Parkinson, who is an enthusiastic proponent of the view that a renewable energy revolution is rapidly undermining the business model of traditional utilities.

In an article published on 1 October, Parkinson notes that Ergon Energy announces in its new annual report that the company is moving away from the traditional ‘poles and wires’ approach to investment because renewables and battery storage are rapidly gaining ground on grid power.

“Will we see a time in the next decade where renewables and battery storage will be cheaper than grid power for the domestic consumer?” asks Ergon Energy chairman Malcolm Hall-Brown half-rhetorically in the company’s annual report.

“The pace of change in the last five years has been dramatic and will likely accelerate, not slow”

Not that renewables are having an easy time of it Queensland. The extensive Queensland grid is subsidised through a uniform, taxpayer-funded subsidy. This means that every household has to pay for it regardless of the amount of electricity people use. At the same time, the generous feed-in-tariff that until recentlyexisted for solar power has been removed. Nevertheless, Ergon Energy notes that an increasing number of householders is turning to solar power “for certainty and control over costs”.

As a result, Ergon sees its role in the electricity market changing: “The network’s role is transitioning from a transporter of electricity to a market enabler”, writes Ergon Energy’s CEO Ian McLeod. “Our customers are increasingly becoming producers selling energy into the grid while changing their consumption behaviours to maximise their return on investment – 14% of households in regional Queensland now have solar.”

Parkinson notes “that capital investment and technology is now flowing downstream into the customer installations – away from traditional regulated infrastructure to unregulated solutions funded by customers or third parties.” As McLeod puts it: “Alternative energy solutions will set a market-based benchmark in pricing as they become increasingly technically and commercially viable. In this environment the network is no longer a monopoly as it delivers a single commodity that can and is already being supplied via other means. This change means our value proposition needs to shift to enable a strong market for energy, storage and demand management solutions, while still providing a safe, secure and reliable supply.”

Interestingly, Queensland’s state-owned generator Stanwell Corp and Energex, the network operator in south-east Queensland, both complained bitterly recently about the effect of solar power on their business, notes Parkinson. Where Ergon sees opportunity, Energex – likewise a state-owned company – sees solar as a threat to its business model.

Energy Darwinism

In a follow-up article on 2 October, Parkinson notes that “The opposing positions of Energex and Ergon, despite their common shareholder is, in many people’s view, a perfect illustration of the sort of choices and challenges being thrust in front of utilities – network operators and generators – in Australia and across the world.”

It is clear on which side Parkinson is on. He cites numerous sources to support his view, including reports from Deutsche Bank, UBS and Citi that are extremely upbeat on the prospects of solar (or conversely, downbeat on the fossil fuel sectors).

“While wind’s intermittency is an issue, with more widespread national adoption it begins to exhibit more baseload characteristics”

Most revealing is a major new report written by the six managing directors of research of Citi’s mining, oil and gas, utilities, commodities and alternative energy sectors, called “Energy Darwinism – the evolution of the energy industry”. The Citi analysts write that “the global energy mix is shifting more rapidly than is widely appreciated, and this has major implications for generators, utilities, and consumers, and for exporters of fossil fuels such as Australia”.

Citi’s report is “a clarion call to review the estimated $37 trillion that will be invested in energy infrastructure and projects over the coming two decades”, notes Parkinson.

Parkinson quotes the Citi report as saying that ‘consumers face economically viable choices and alternatives in the coming years which were not foreseen 5 years ago’, pointing mostly to the “alarming” falls in the cost of solar.

The Citi analysts say “the pace of change in the last five years has been dramatic and will likely accelerate, not slow. These changes will flow through to suppliers. Conventional fuels and technologies are likely to be substituted, or suffer reduced demand in the best case scenario.”

The Citi analysts note that “fossil fuels further up the cost curve are most at risk, and new projects built now will face competition with new technologies within the first quarter of their anticipated 25-year life. These project entail significantly more risk than is widely recognised.”

European utilities

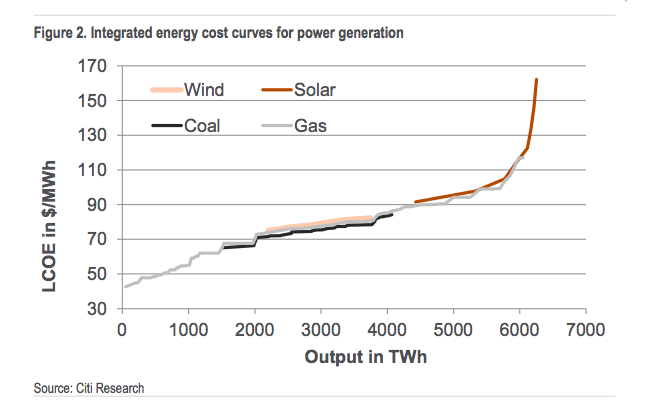

Parkinson reproduces a crucial graph from the Citi report that compares the cost of wind power, solar power coal-based and gas-based electricity generation:

He explains the graph as follows:

“In the first quartile it notes that gas (the light grey line) dominates the first quartile of the integrated cost curve, largely thanks to the advent of shale. So that is probably true of the US, but not many other places (in Australia, gas is really expensive, or about to be). The key is what happens in the other quartiles.”

“In the final quartile, it notes that solar is already intersecting with gas, which is why utilities in the US are dumping plans for peaking gas stations in favour of solar (red line). And this also means that solar steal the most valuable part of the electricity generation curve because it produces during the day when prices are highest.”

“This is already impacting Germany, where gas is expensive and gas-fired generators are going out of business, and it might have cited Australia too, where returns for incumbent fossil fuel generators are falling dramatically and so it their running time. Wind farms such as Collgar in WA are running at higher capacity factors than black coal generators in NSW.”

“Citi notes that wind (orange line) is already overshadowing coal (black) in the second quartile. But here’s the conclusion that will stun those locked into a conventional view of generation: Citi says that while wind’s intermittency is an issue, with more widespread national adoption it begins to exhibit more baseload characteristics (i.e. it runs more continuously on an aggregated basis). ‘Hence it becomes a viable option, without the risk of low utilisation rates in developed markets, commodity price risk or associated cost of carbon risks’.”

Citi strikes an especially alarming note on the challenges facing European utilities: “If we look at the situation facing European utilities, the future looks particularly challenging, given a potential halving of their addressable market, an ageing fleet, and deeper questions about what a utility will look like in 5, 10 or 20 years’ time.”

There is a lot more to learn in these articles. Do check for yourself.

By Giles Parkinson on the website Reneweconomy.com.au:

Ergon says renewables and batteries may be cheaper than grid, 1 October

Electricity utilities could lose half their market to solar and storage, 2 October

Energy Darwinism: Fossil fuels and utilities at risk, 2 October

The decline of baseload: is solar about to claim another victim, 3 October