RWE’s lignite mine Inden in Germany (photo: Glasseyes View)

RWE has posted its first loss since World War II. Everyone – not only proponents of renewables – now claims that the firm’s management failed to see how renewables would affect its bottom line. That’s true, but even if they had, what should they have done? More importantly, what should they do now?

German economics daily Handelsblatt says RWE’s predicament is not its current CEO’s fault (Peter Terium), but the fault of the previous one, Jürgen Großmann, who left the firm a “dinosaur.” Der Spiegel, which complains about everything, disagrees, saying that Terium’s “strategy is complaining.” (Talk about a crow calling a raven black…)

So what exactly should the firm have done? Let’s play a little game – it’s 2000 (the year in which the German government adopted its Renewable Energy Act and the nuclear phaseout), and you are the CEO of RWE. I’m going to be the chairman of the supervisory board and tell you whether your ideas are good or bad.

The new feed-in tariffs (like the old ones) are available to everyone, so RWE can take advantage of them. You would like to invest in renewables. I’m not so sure. The return is estimated at 5-7 percent. Our capital is limited, and we are generally not happy getting less than 10 percent. Why settle for half as much?

Furthermore, we are entering the era of liberalized markets. Power firms used to sit down with the government and negotiate prices to prevent customers from being gouged – but in return, our profits were practically guaranteed. (How else do you think we managed to post a profit every single year for seven decades?) These feed-in tariffs, however, do not guarantee anything. We might get five percent, or we might lose money.

And have you thought about how renewables are going to hurt our current assets? The more we invest in solar, the more peak demand at noon time will be wiped out, which will affect our gas turbines. And wind power is produced wildly day and night. If we get too much of this (laughter in the board room), it will start cutting into the medium load and possibly even the baseload at times of low demand, such as at night – then, our coal and nuclear plants are also affected.

The board agrees not to invest in renewables (and you justifiably leave the room in a sweat, aware that we have our eye on you now…).

Fast-forward to 2005. Since last year, feed-in tariffs have been offered without limits for photovoltaics, but still only a few hundred MW a year is being installed. The wind market peaked in 2002 and has slumped noticeably since. You still think we should take renewables more seriously, but we inform you of some more urgent problems that need addressing.

Emissions trading just got started, and we are awash in cash; the allowances were handed out for free, and we have a lot of liquidity to invest. However, by 2016 most coal plants in Europe will have to close because of new emissions standards. You timidly suggest that wind, PV, and biomass could replace some of that capacity, but board members only roll their eyes and say new coal plants that fulfill these new standards should be built. Your next suggestion does make us think, however – the carbon price could go up over the next few decades, making these investments in new coal risky.

You sure got the board’s attention! But after a lengthy discussion, it is agreed that the nuclear phaseout and the new emissions standards for coal plants will simply remove too much baseload power, so investments should be made in new baseload capacity.

Fast-forward to February 2011. The economic crisis means that all bets are off. The price of carbon is headed down. Wind turbines continue to be installed at a rate of just under 2 GW per year, but solar just exploded – in 2010, around 7.5 GW was installed. Even the German Environmental Ministry has been caught with its pants down. In its “Leitstudie” (essentially, the master plan for the Energiewende, which is updated every year) of 2008 (PDF in German), they expected 7.7 GW of PV to be installed by the end of 2010 cumulatively (see Tabelle 5). By 2050, the BMU believed Germany would have 29.0 GW of photovoltaics installed (which we had in 2012).

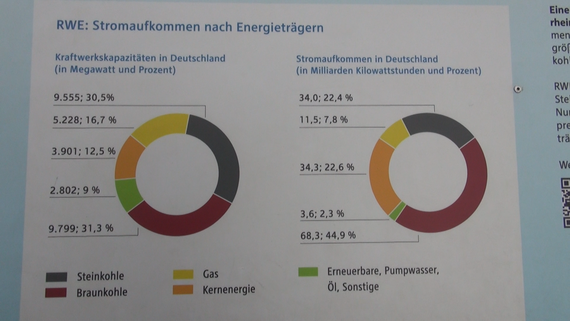

Visitors to Garzweiler, a giant openface lignite coal field near Cologne, get to see this old chart showing that renewables (the green slice of the doughnut on the right) make up 2.3 percent of the firm’s power supply, compared to 44.9 percent lignite and 22.4 percent hard coal. The company now has slightly more renewable electricity, but only around four percent. But the figures for Germany as a whole in 2013 look a bit different: 25 percent renewables, 25 percent lignite, and 20 percent hard coal.

But in the Leitstudie 2010 published this month (February 2011), the BMU changes its tune. The Ministry now expects new PV installations to taper off at around 3.0 GW annually until 2030 (see Tabelle 10.12 of this PDF in German). But because of the current boom, Germany would have around 35 GW installed at the end of 2014, more than expected by 2050 just a few years ago.

(You keep an eye on the Leitstudie, so you later notice that the version of 2011 (PDF in German) no longer contains the table from the 2010 version (Table 6.2) showing expectations for rising wholesale power prices, which are now dropping. I guess the experts didn’t see that coming until it was too late either…)

In 2009, I spotted my first Tesla in the wild at RWE’s headquarters in Essen. I visited the firm to speak to the directors of the company’s demand management pilot project for retail customers. Think large utilities should be looking into offering shifting hourly rates to reward consumers who shift power demand with appliances like refrigerators at home? They have all been looking into it for years. The main finding is that a large majority of German customers are outright hostile to the idea.

You propose that we begin diversifying, not only by investing more in renewables, but also by building up the enabling infrastructure – such as charging stations for electric vehicles. “But there are practically no electric vehicles on the road,” one board member objects. Another points out that, as a power provider, we can hardly influence supply and demand for electric vehicles. Still, we are beginning to realize you might have been right all along. You had us look into Teslas back in 2009, and all the board members loved riding in it, so we like you more with each passing year.

Still, between the unexpected boom in PV, the unexpected drop in wholesale prices, the unexpectedly low carbon price, and the financial crisis, all bets are off – the board resolves to stop all new coal projects that can still be held back and not to start any new ones. We are all the more tepid about renewables now that we see the havoc that PV is going to wreck on our peaking plants. (No laughter on the board.)

Let’s not forget that at the end of 2010 the German government extended commissions for nuclear plants by 8-14 years, which we celebrate at our board meeting in February 2011. Little do we know that, in a few weeks, the German government is going to force us to shut down a number of our nuclear plants immediately.

We’ll stop this game now; I hope I’ve made my point – there is a certain logic to the conventional utility business model, and those expressing schadenfreude about RWE would hardly have navigated the firm better. We would have all failed in two ways.

First, investing in renewables was never in the interest of energy corporations. The reason why Germany succeeded in ramping up renewables is because they understood this and came up with a policy that would allow others to make these investments – citizens, energy co-ops, municipals, etc.

Second, no one expected PV to grow this fast. The sudden boom of PV has been much more disruptive than the more gradual growth of wind and biomass. I didn’t see this coming, Peter Terium didn’t, and the German Environmental Ministry didn’t. I’d wager that none of the people complaining about RWE’s shortsightedness can paste in a link in the comments below demonstrating that they knew we would be where we are today five years ago.

What should RWE do? I don’t know, and I don’t see too many good suggestions out there elsewhere – but go ahead, put yours in the comments below. Maybe we need to be open to the idea that large power corporations were needed for central-station power plants, but that their role in a renewable future will be much smaller. At the moment, even the proposal to have them leverage their size to set up an enabling infrastructure – such as charging stations for electric cars – seems unlikely. The firms don’t even have the liquidity anymore. (Craig Morris)

About the author

Born in the United States, Craig Morris has been living in Germany since 1992 and working in the renewables sector since 2001. In 2002, he founded Petite Planète, a translation and documentation agency focusing on renewables. He is the author of two books in German and English, has served as editor of several energy magazines, writes for the Energiewende Blog (Energy Transition.de) and writes daily at Renewables International. This article was first published at Renewables International. Craig has generously offered to share it with Energy Post. All rights reserved.

Editor’s Note

For more information on RWE’s strategic conundrum, see this article on Energy Post that we published last year and which is based on confidential strategy documents that were discussed at a Supervisory Board meeting of RWE. We soon hope to follow up with an interview with RWE’s CEO Peter Terium.

A solid effort to defend RWE’s decision making, but one only has to look at E.ON’s recent financials – a €2.2bn profit versus RWE’s €2.8bn loss to doubt it. E.ON did invest in renewables, RWE thought coal, CCS and nuclear were the future.

One must wonder if RWE really could and should have done better…..

Perhaps RWE’s best bet now is to sue for bankruptcy?

RWE still has substantial revenues (E50bn I believe). One route could be reduce the size of the company & re-focus. Not comfortable, not easy but a possible survival route.